Montgomery, 9-0.

I called this a catalyst. The Court just made it a scramble.

Three weeks ago I wrote that Montgomery v. Caribe wasn’t going to kill freight brokers, but it was going to kill the model. The transactional, procedural, paperwork-driven version of brokerage that has run this industry for forty years. I said the legal outcome was almost beside the point: insurance markets, sophisticated shippers, and fraud were going to force the infrastructure buildout regardless of how the Court came down.

I expected a narrow ruling. Something in between. A decision that left brokers exposed enough that they couldn’t ignore the problem, but didn’t give them clean instructions either.

The Court didn’t go narrow. The Court went 9-0.

Justice Barrett, writing for a unanimous bench, held that negligent-hiring claims against freight brokers fall squarely within the F4A’s safety exception. The phrase “with respect to motor vehicles” includes the broker who hired the carrier driving the vehicle. State tort suits proceed. C.H. Robinson goes back to the Seventh Circuit as a defendant. Every broker in the country just woke up to a different operating environment than the one they went to bed in.

So let me update the priors.

What I had right

The catalyst framing held up. Montgomery is now the trigger that forces every other pressure including insurance repricing, indemnification clauses, fraud exposure, fleet-level visibility and to compound on a faster clock. The mortality curve is still a tide, not a cliff. No broker is closing today because of Barrett’s opinion. But the tide just doubled in speed.

The “should you have known” standard is now black-letter law. That was the entire substantive question I flagged in April: when the legal regime moves from procedural compliance (did you check the boxes) to substantive duty (should you have known better), the answer gets settled by data or by its absence. The Court just made that the rule.

The infrastructure case held up. The brokers who survive will be the ones who can document what they knew, when they knew it, and why they made the call they made. Everything else is rationalization.

What I had wrong or at least, underestimated

I expected a 6-3 split. Maybe 5-4 with Barrett as the swing. The questioning at oral argument suggested at least two justices were sympathetic to the brokerage industry’s preemption argument, and Kavanaugh’s concurrence (joined by Alito) confirms it, they openly say the case was closer than the majority opinion suggests, and that several contextual points “favor the brokers.”

They concurred anyway.

That’s the part the industry should sit with. Even the justices who saw the brokerage argument couldn’t write a coherent path to preemption. The statutory text didn’t give them one. “With respect to motor vehicles” is elastic enough to swallow negligent-hiring claims, and once you concede that, the rest of the analysis is housekeeping.

The 9-0 isn’t just a loss. It’s a signal that there is no legal cavalry coming. No future case is going to roll this back. The TIA can lobby Congress to amend F4A, but that fight takes years and the votes aren’t obvious. In the meantime, the operating model has to change.

I also underweighted how quickly this would arrive. I expected late June. We got mid-May. That’s six weeks of additional liability exposure baked into every load underwritten between now and Q3 renewals.

The 3 questions just got harder

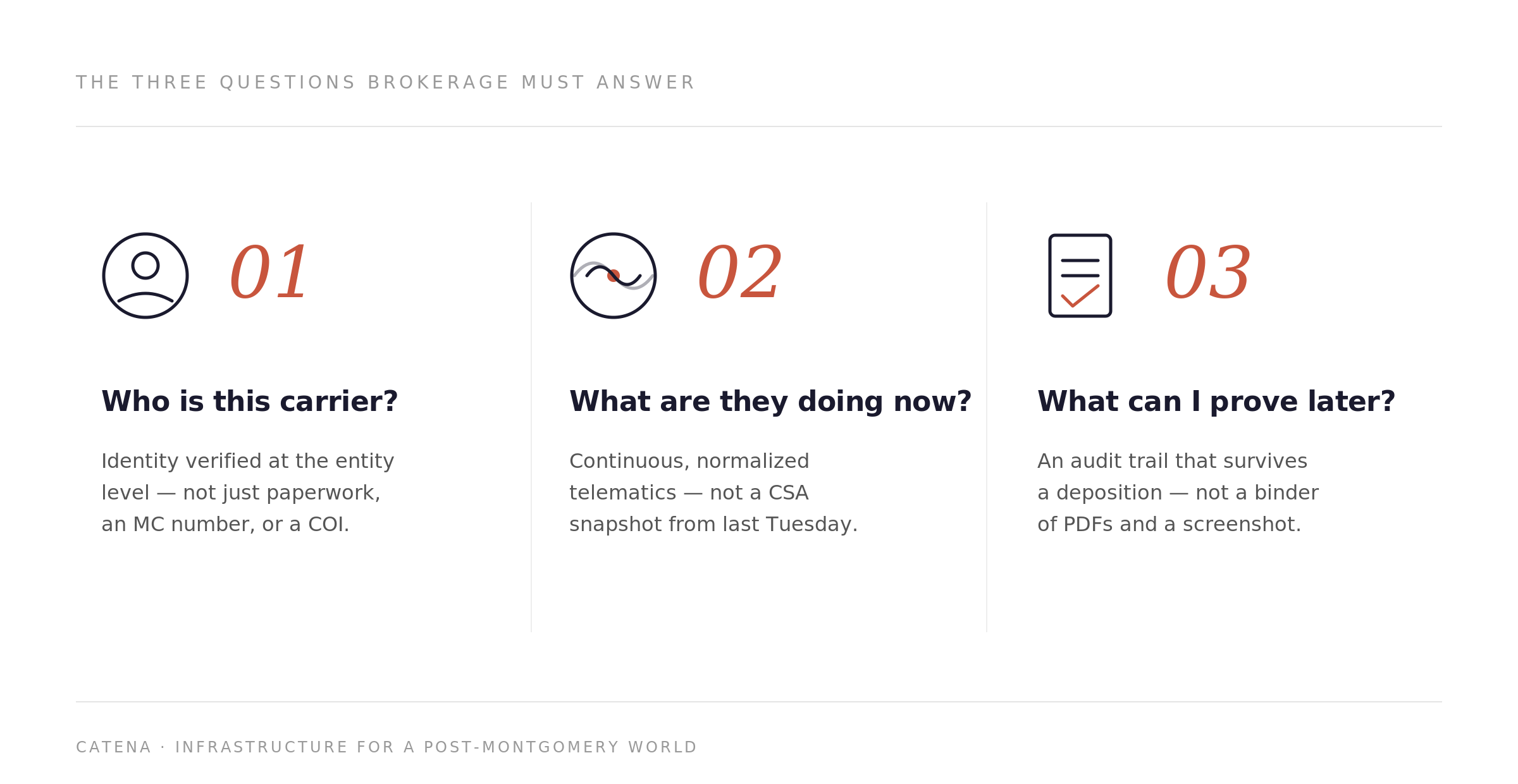

I argued in April that the infrastructure layer brokerage needs has to answer three questions on demand:

Is this carrier who they say they are?

What are they actually doing right now?

Can I prove, after the fact, what I knew and when I knew it?

Pre-ruling, those questions were a competitive advantage. Brokers who could answer them won better insurance rates, better shipper contracts, fewer claims.

Post-ruling, they’re a defense. The broker who can’t answer them confidently, with audit trail, in real time is the one writing settlement checks. And in a 9-0 world, settlement checks aren’t getting cheaper. The plaintiff’s bar just got handed a roadmap. Every accident involving a carrier with a marginal safety profile is now a viable suit against the broker who hired them. Every double-brokered load where the entity that picked up isn’t the entity that was vetted is a discovery question waiting to be asked.

The brokers who can produce continuous, signed, time-stamped operational data on the carriers they dispatched will be in a fundamentally different defensive position than the brokers who can produce a CSA snapshot from sometime that week. That’s not a marginal advantage. That’s the difference between a case that gets dismissed on summary judgment and a case that gets to a jury.

Fraud just became a board-level issue

I made the point in April that the conversation around Montgomery is mostly about negligent selection of legitimate carriers, and that this misses the larger problem: a meaningful share of the worst outcomes in freight come from the broker hiring a carrier that wasn’t actually the carrier they thought they hired.

That argument was true before today. After today, it’s existential.

ATRI’s last estimate put annual freight fraud at $6.6 billion. Widen the aperture to identity spoofing, double-brokering, and supply-chain crime and Homeland Security puts the number at $35 billion. Cargo theft rose 27% in 2024 and another 22% in 2025. None of those numbers care about preemption.

What changes today is the legal consequence of not knowing who actually moved your load. Pre-Montgomery, a broker who couldn’t conclusively prove the identity of the dispatched carrier was running a fraud risk. Post-Montgomery, that broker is running an unliquidated tort liability that an underwriter will price into next year’s premium assuming the underwriter agrees to write the policy at all.

Identity verification stops being a fraud-prevention nice-to-have. It becomes the foundation of every defensible carrier selection in the country.

Why this is the moment Catena was built for

I’ll be direct about this part, because it’s the through line from the April post to today, and our investors and customers should hear it from me.

The reason we started Catena was the bet that freight was going to need a connectivity and verification layer that no individual broker, carrier, or TMS could build on their own. The data needed to operate in a post-Montgomery world is fragmented across hundreds of telematics and ELD providers, dozens of compliance vendors, and the brokers’ own internal systems. The unit economics of any one company assembling that picture from scratch at the scale and freshness that a “should you have known” standard demands don’t work.

That’s the layer we’ve spent the last two years building. 900,000+ vehicles. 200+ telematics and ELD integrations. Canonical identity for every vehicle, driver, and fleet across providers. Real-time visibility, normalized to a single API, with the audit trail intact. Today is not the day we change our roadmap. Today is the day the market’s roadmap converges with ours.

Three things follow from the ruling, all of which are good for the infrastructure we’ve already built:

Insurance markets reprice fast. Underwriters have been waiting for this decision to lock in their 2027 cycle. The brokers who can document carrier selection with normalized, continuous, third-party-verified data are going to get rates the brokers who can’t won’t. That repricing creates a wedge that converts our product from competitive advantage to procurement requirement.

Shippers push risk down. Walmart, the Apexes of the world, the large 3PLs anyone with leverage is going to start writing indemnification language that demands documented carrier vetting. The brokers who can prove their process win the freight. The brokers who can’t lose it. Catena is what makes the proof possible at scale.

Fraud surface contracts. Every layer of carrier identity verification we provide FMCSA enrichment, persistent canonical IDs, real-time first-party telematics handshake closes a door that the spoof economy has been walking through. In a 9-0 world, those doors don’t just cost money to leave open. They become legal liabilities.

We weren’t waiting for this ruling. We were betting it didn’t matter for the long-term thesis. It didn’t. But today’s outcome compressed the timeline on which the industry catches up to the thesis, and the part of the market that was happy to keep operating on procedural compliance just lost that option.

What to actually watch from here

A few signals to track in the next 90 days that will tell you whether the industry is internalizing the ruling or trying to litigate around it:

The C.H. Robinson Q3 earnings call. Bob Biesterfeld will be asked, on the record, what changes operationally. The answer matters less than the framing: confident and prepared signals the industry is moving; defensive and procedural signals it isn’t.

The TIA’s legislative posture. If the trade association pivots quickly to seeking an F4A amendment, it’s a tell that they don’t think the carrier-vetting infrastructure can be stood up at the pace the courts will demand. That’s the right read.

Insurance renewals at Q3/Q4. The first wave of brokerage E&O and auto liability renewals after the ruling is the cleanest market signal you’ll get on what the new risk looks like priced in. Watch for tiered rates based on demonstrable carrier vetting that’s the world we’ve been describing for two years.

State tort filings. The plaintiff’s bar moves fast. Expect a wave of new filings against brokers in the Seventh, Ninth, and Sixth Circuits within 60 days. The fact patterns of those filings will tell you which brokers by size, by tech stack, by data posture are the most exposed.

The real outcome, updated

The April post argued the model was dying the procedural, paperwork-driven version of brokerage that has run the industry for forty years was on borrowed time, and infrastructure was what replaced it.

Today the Court put the end date on the calendar.

Some brokers will make the transition. Most won’t. The ones that do won’t do it alone, because no broker has the surface area to build the data layer they’ll need. That layer was going to get built either way. The case just set the timeline.

The timeline is now.